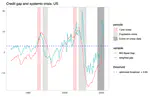

Implements model averaging to improve the performance total credit gap as a predictor of financial crises. The model uses quarterly panel data of 50 years across 40 countries. The methods used are Bayesian model average, partial Area under the ROC curve (pAUC), index synthesizing, n-fold cross-validation, and policy function optimization.